EU report signals breakthrough moment for CCU technologies

The European Union is accelerating its efforts to become a global leader in carbon capture, utilisation and storage (CCUS) technologies, according to a new report by the European Commission’s Joint Research Centre (JRC). The 2024 edition of the status report reveals an industry on the cusp of large-scale deployment, driven by stronger policy support, technological progress, and a growing portfolio of investments across Europe.

In 2023 alone, the global CCUS sector more than doubled its development pipeline, with projects now capable of capturing over 360 million tonnes of CO₂ per year. While 41 commercial-scale CCUS facilities are already operational—mainly in North America and Europe—experts say the technology’s full potential is still untapped, especially in hard-to-abate industrial sectors like cement, steel, and chemicals.

The report positions CCUS as a key component in the EU’s strategy to meet its 2050 climate neutrality goals. “CCUS is not just a complementary technology—it’s an essential pillar of industrial decarbonisation,” the report states. This is underscored by recent EU policy actions. In May 2024, the Council adopted the Net-Zero Industry Act, which designates CCUS as a Strategic Net-Zero Technology and sets a binding target to store at least 50 million tonnes of CO₂ annually in EU geological sites by 2030.

The momentum continued earlier this year with the launch of the Industrial Carbon Management Strategy, laying out a roadmap to scale carbon capture from 50 Mt per year in 2030 to 450 Mt by 2050. Much of this growth is expected to come from heavy industry, where emissions are especially difficult to reduce.

Barriers

Despite the surge in project development, the report acknowledges that CCUS remains a costly undertaking. Capture costs vary widely—from €40 to €90 per tonne of CO₂ in industrial applications—while Direct Air Capture technologies can exceed €300 per tonne. Transport and storage costs add further complexity, especially for offshore infrastructure.

Still, optimism is growing. “As capacity increases, costs are expected to fall significantly, aided by modular design, learning-by-doing, and digitalisation,” the authors note. Innovative capture technologies and economies of scale in shared infrastructure, such as CCUS hubs, are expected to play a major role.

Europe steps up

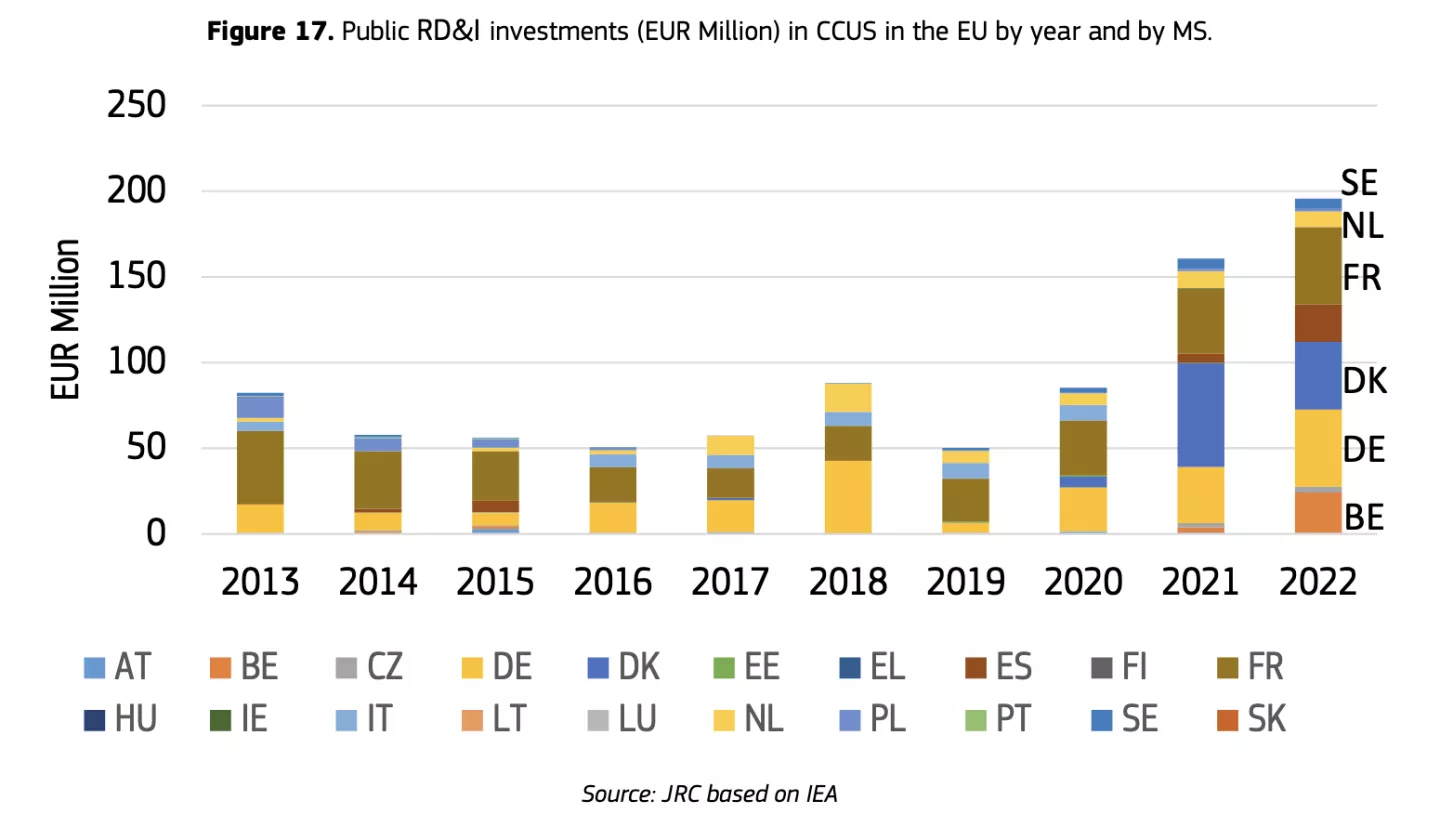

Europe’s strength lies in innovation. The EU was the global leader in public research and innovation (R&I) funding for CCUS in 2022, investing over €4.5 billion across more than 100 projects. Germany, France, Denmark and Belgium led national investments, while EU-wide programmes like Horizon Europe and the Innovation Fund provided critical support.

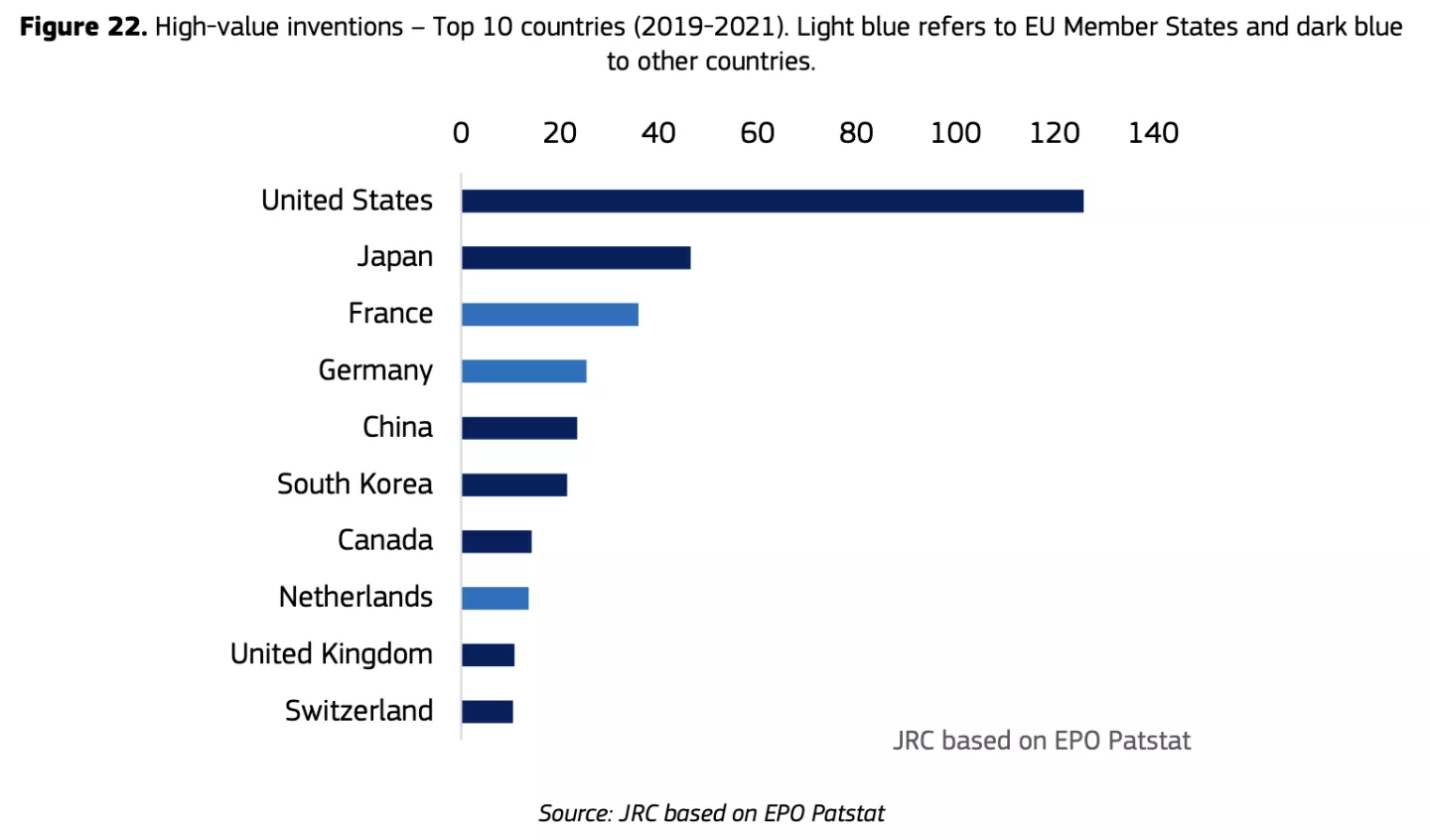

On the private side, EU companies—particularly in France, Germany, the Netherlands and Sweden—rank among the top global patent holders for high-value CCUS technologies. Leading innovators include Air Liquide and Linde, both of which are heavily involved in ongoing CCUS pilot and demonstration projects.

Yet Europe trails behind in venture capital. Only 18% of global VC investment in CCUS went to European firms, compared to a dominant share in the United States. Most new VC-backed startups have emerged since 2020, but the majority are located in North America.

New business models

One of the most significant developments highlighted in the report is the evolution of business models. Traditional “full-chain” projects—where a single operator captures, transports and stores CO₂—are being replaced by more flexible, collaborative approaches. Partial value chain models, such as “capture-as-a-service” or “transport and storage as a service,” enable infrastructure sharing and risk pooling.

Several European hubs are already putting this into practice. The Porthos project in Rotterdam, for example, connects emitters like Shell and Air Liquide to a shared offshore storage site. Other hubs are being developed in Norway (Longship), France (Dunkirk), and Iceland (Coda Terminal).

Supply chains

A final word of caution concerns the materials needed to scale up CCUS technologies. From corrosion-resistant steel to critical raw materials like chromium, vanadium and nickel, the EU’s supply chain remains vulnerable. Many of these inputs are imported from countries like China and South Africa, raising questions about long-term resilience and strategic autonomy.

Turning point

While the United States currently leads in operational CCUS facilities, Europe is carving out a leadership position in research, policy, and industrial applications. The JRC’s 2024 report paints a picture of a rapidly maturing sector—one that holds enormous potential to support the green transition, if supported by smart policy, strategic investment, and cross-border cooperation.

For Flanders, this report is both a call to action and a validation of ongoing regional efforts. As industrial clusters prepare for net-zero, CCUS will likely become a central part of the solution mix.

Figures from the report